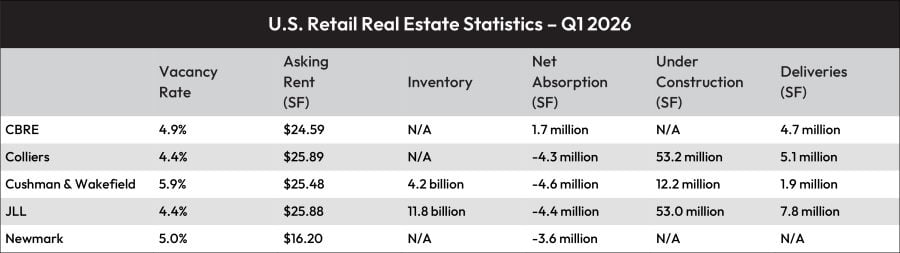

The Q1 2026 retail experiences agreed on a number of issues. First, destructive internet absorption charges have been reported throughout all 5 write-ups, with the lone exception being CBRE’s “U.S. Retail Figures.” Nonetheless, “a number of chapter filings triggered a wave of closures, which added obtainable house to the market,” the CBRE analysts defined.

Second, these chapter backfills are being snapped up by what Colliers “U.S. Retail Figures” write-up known as regular demand, including {that a} “clear bifurcation persists, with tight availability for spall areas and extra modest availability amongst massive anchor bins.

Third, the development pipeline continues to dwindle. JLL, in its “Retail Market Dynamics” report, mentioned that gross deliveries of seven.8 million sq. ft have been “partially offset by 2.6 million sq. ft of demolitions, comprising out of date shops and underperforming strip facilities. In consequence, internet new provide “equated to roughly 5.2 million sq. ft for the quarter,” the JLL analysts mentioned.

Extra causes got for flat hire development and destructive absorption. Newmark’s “Retail Market Conditions & Trends” mentioned that market uncertainty didn’t assist issues as “client sentiment continues to be negatively affected by lingering inflation, uncertainty concerning the job market and the impression of the Iran battle on gasoline prices and doubtlessly different costs.” Nonetheless, Newmark analysts and others mentioned that retail gross sales and client spending stay in constructive territory.

In the meantime, Cushman & Wakefield’s “MarketBeat” mentioned that first quarters are usually slower for retail leasing, whereas “extreme winter climate could have curtailed exercise greater than regular this yr.”

As for the outlook, all of the experiences mentioned that continued provide shortages will proceed to exert stress on hire development. On the identical time, client sentiment is value maintaining a tally of. “If elevated oil costs persist, larger prices for gasoline, utilities and client merchandise are more likely to weigh on family budgets and client confidence in Q2 and doubtlessly longer,” mentioned Cushman & Wakefield analysts.

JLL added that the provision scenario isn’t more likely to change anytime quickly, including that “location will matter greater than the nationwide common.” All of the experiences mentioned that the Solar Belt markets outpaced the remainder of the nation in retail metrics, pushed by inhabitants development. “For the rest of 2026, efficiency can be much less concerning the market total, and extra about which markets a portfolio is in,” JLL researchers added.

Colliers forecast that restricted provide, mixed with sturdy demand, means a fast backfill, although Newmark analysts famous that backfill exercise isn’t exhibiting indicators of slowing.

Newmark added that stagnant, older retail house might make the case for extra retail development. However with development prices nonetheless excessive and rents unable to justify new improvement, alternatives might exist in redeveloping underperforming facilities “by means of redesign or mixed-use conversion,” which is able to take away outdated house from the market and “finally cut back the entire retail footprint,” Newmark researchers mentioned.

In the meantime, as retailers are more likely to stay cautious about near-term leasing whereas they monitor client circumstances, Cushman & Wakefield researchers indicated {that a} broad pullback is unlikely.

“Assuming easing power costs and a resilient labor market with solely modest unemployment will increase, retail demand ought to stay resilient, supporting emptiness stabilization by means of year-end,” they added.