Take the luxury-sports-car view of family wealth.

For roughly 10 years, I had a used, triple-black midlife disaster Porsche Boxster S convertible that introduced me hours of pleasure however was admittedly pedestrian within the luxurious sports-car world. I’m going to make use of an actual sports activities automobile within the software of a correct analogy of the surge in family wealth. I’ll clarify.

This weekend we stayed with associates within the Hamptons (on jap Lengthy Island), largely a second residence luxurious market east of New York Metropolis, and took a tour of all of the homebuilding occurring on the market and consider me it appears so much higher from the passenger seat of a 1988 Porsche 911 Carrera with the M491 “Turbo Look” choice, operating the inventory G50 5‑pace, whose authentic 3.2 flat‑six has been rebuilt and enlarged to three.4 liters. (translation: it’s fast and hugs the highway). But I didn’t see a single Porsche Boxster S all weekend. The sheer variety of luxurious automobiles and high-performance sports activities automobiles, together with the huge scale of latest development for the reason that pandemic started, is tough to course of. Zipping round hamlets reminiscent of Westhampton Seaside, Westhampton, Quogue, and Hampton Bays, it was truthful to counsel that at the very least 50 p.c of the housing inventory has been both considerably upgraded or torn down and changed with properties two-to-three occasions bigger for the reason that lockdown. How is the huge scale of this new development even sustainable? Then think about the right second of high compensation for Wall Street, set alongside the surge in family wealth for the reason that pandemic started and the dominance of money patrons.

However why did family wealth rise a lot?

Each the monetary markets and actual property have contributed considerably to the explosion of family wealth for the reason that pre-pandemic period, on a scale not skilled earlier than.

This surge in wealth, expressed by way of the housing inventory (and sports activities automobiles), is clearly Wall Street-related, as defined in my first-quarter Hamptons market analysis, however it’s not the one driver of this market.

The pandemic-era surge in family wealth was pushed by an uncommon mixture of compelled saving and an enormous asset-price increase in housing and equities, all layered atop inequality that has been increasing for years worldwide. An interesting snippet from the IMF again in 2021, as we exited the darkish days of Covid:

Family saving elevated sharply through the COVID-19 disaster in lots of nations. Decrease consumption, each on account of lockdowns or precaution, mixed with a rise in disposable earnings from authorities transfers allowed households to place more cash into their financial institution accounts, purchase shares, a home, or pay again their debt. Together with saving, surging fairness and housing costs additionally made sure households so much wealthier.

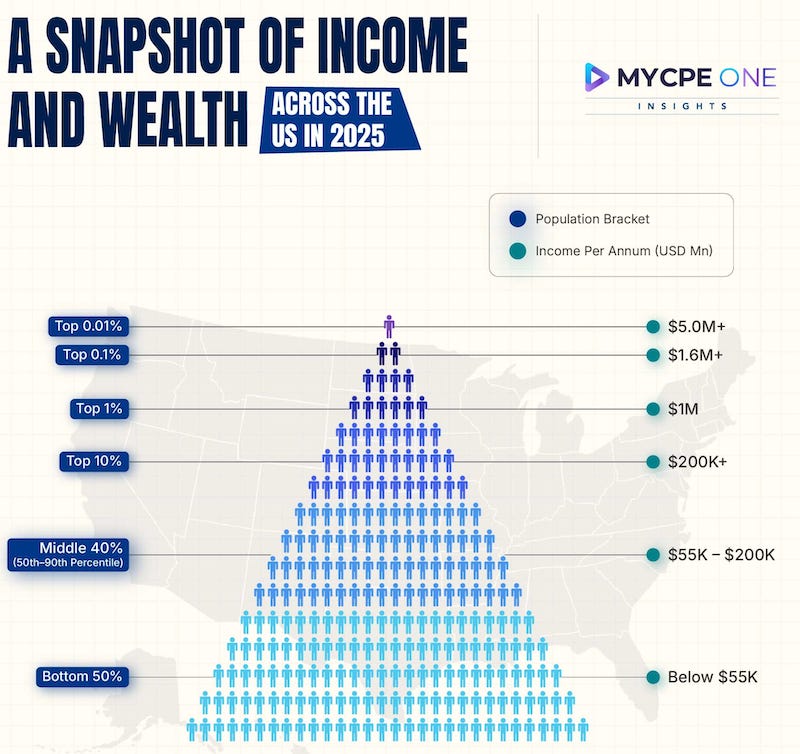

Family metrics of the highest 0.1 p.c

The highest 0.01 p.c of the wealth distribution accounts for almost 140,000 U.S. households, who, in line with the Fed, every have a web value of almost $190,000,000. The wealth of the general inhabitants has expanded by about 8x since 1989, whereas the highest 0.1 p.c has elevated greater than 13x, illustrating simply how a lot quicker the .01% group’s property have grown than the rest.

Beyond the income itself, what’s most attention-grabbing about this evaluation is that their wealth is rising a lot quicker than the variety of people. In reality, over the previous few a long time, the highest 0.1 p.c have gained wealth quicker than the highest 1 p.c total, which in flip have gained quicker than the highest 10 p.c, whereas each have outpaced the center 50–90 p.c and the underside 50 p.c in relative phrases. The historical past that kinds this sample makes me suppose it received’t finish anytime quickly.

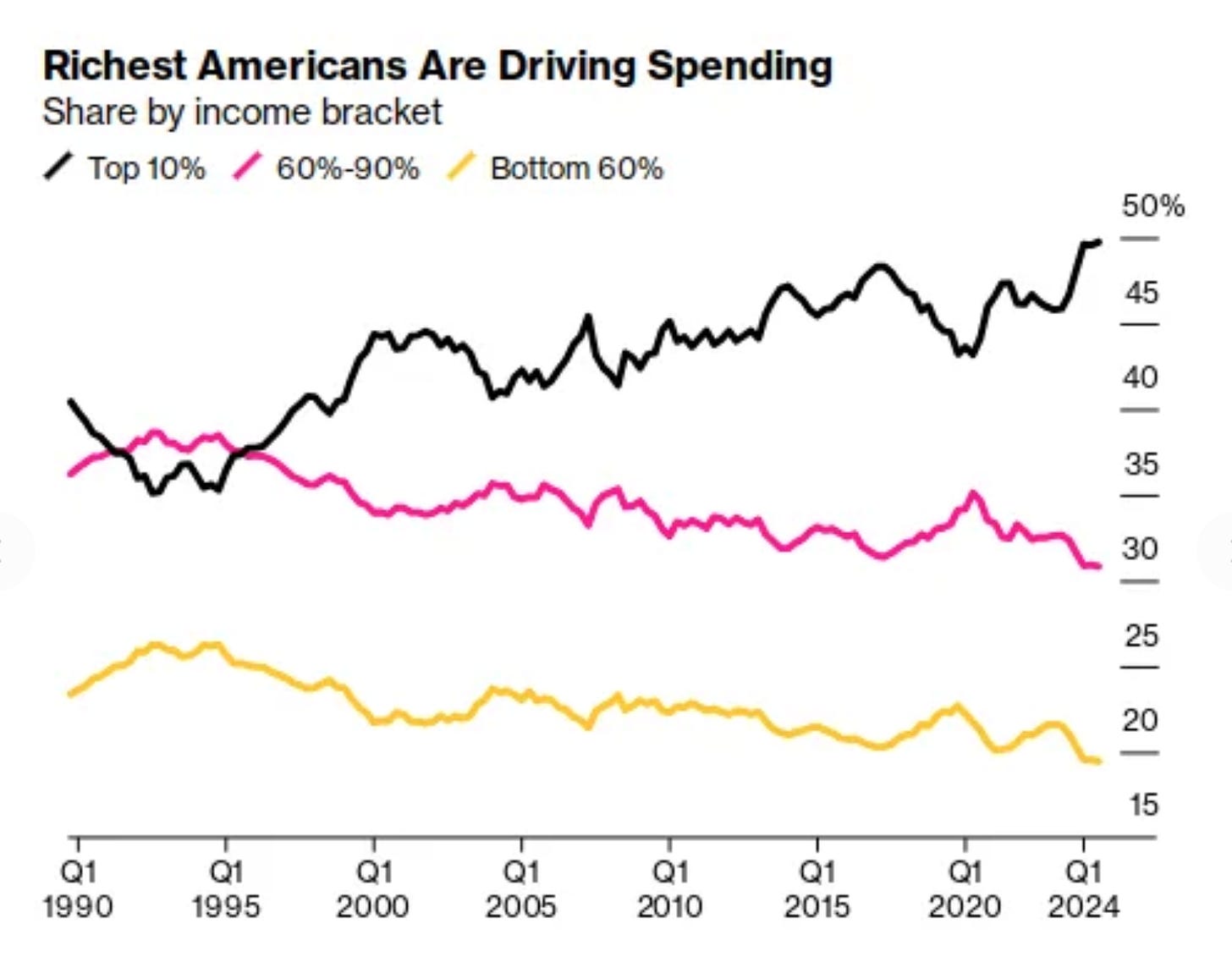

Be aware using the phrase “driving” right here.

Supply: Bloomberg

Remaining ideas

There was a structural shift in housing, during which the highest finish features extra as a luxurious asset than as shelter, with speedy teardown cycles and upsizing resetting market norms. It additionally displays a decoupling from native fundamentals, as cash-heavy, finance-driven patrons maintain demand and scale back sensitivity to rates of interest, probably prolonging the cycle.

The precise last thought — A type of resiliency for retail you’d by no means count on.

Learn extra Housing Notes columns and join e mail newsletters here.

Learn extra

Housing Notes: Wall Street is adding more finance jobs to NYC than anywhere else

Luxury new development deals climb to 10-year high